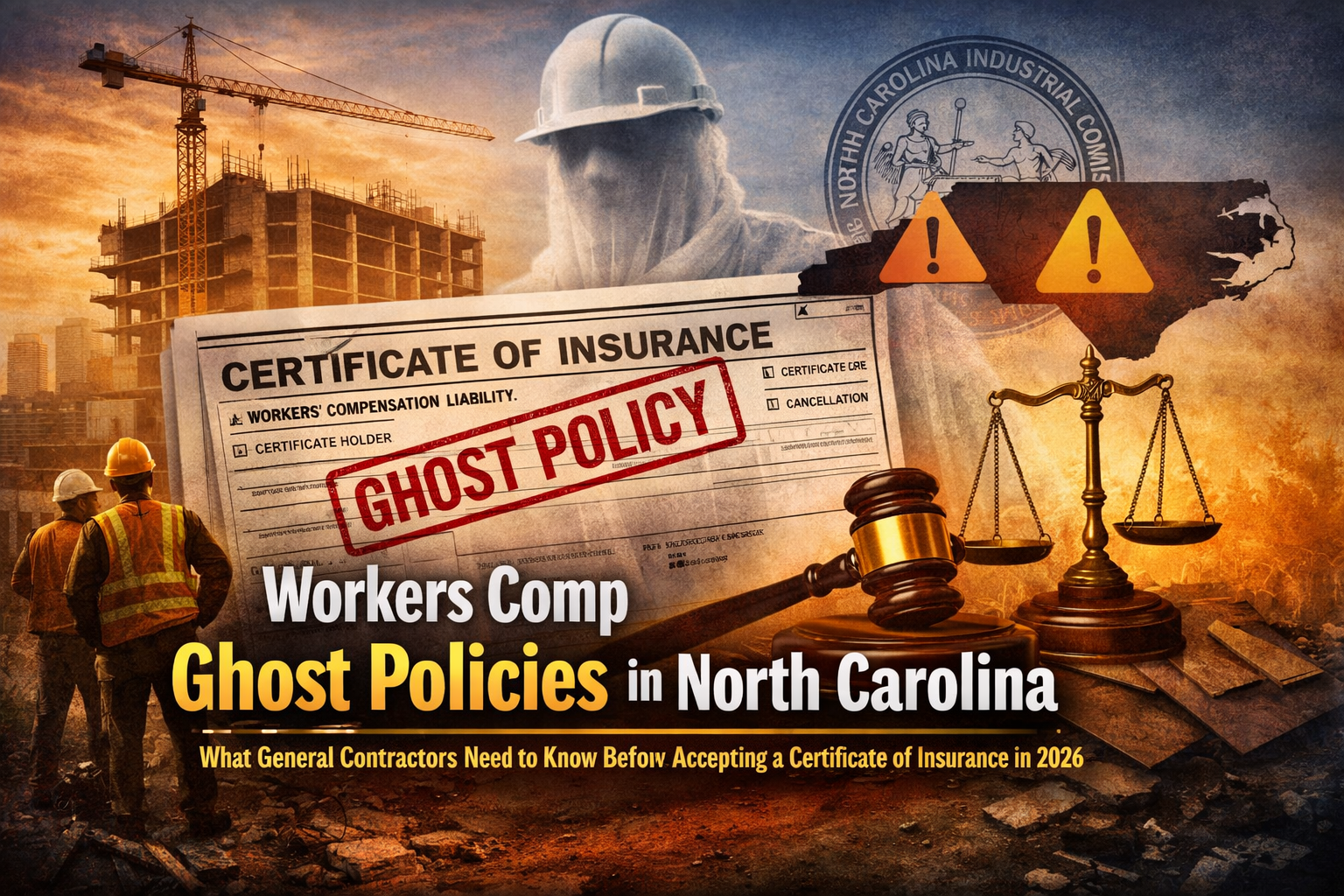

Workers Comp Ghost Policy North Carolina Guide for General Contractors

A workers comp ghost policy can look valid on a certificate while leaving the actual job site labor uncovered. For North Carolina general contractors, that gap can become your problem after an injury.

- A workers comp ghost policy is a real policy that may cover no actual workers.

- A certificate of insurance can show that a policy exists, but it does not prove who is covered.

- North Carolina general contractors can face exposure under N.C.G.S. § 97-19 if a subcontractor lacks workers comp coverage that responds.

- Owner exclusions, zero payroll, and missing class codes are warning signs that need verification.

- Coverage should be verified before the subcontractor starts work, not after someone gets hurt.

A workers comp ghost policy in North Carolina is a real workers compensation policy that may cover no actual workers. The certificate may look valid, but it may not cover the owner, the crew, or the people doing physical labor on your job site.

- What is the trap?

- The policy can pass the paperwork test while failing the claim test.

- Why should general contractors care?

- If a subcontractor worker gets hurt and the sub has no real workers comp coverage, the claim may move up the chain.

- What should be checked?

- Owner exclusions, covered payroll, class codes, active policy status, declarations page, and carrier verification notes.

The certificate looked fine. The policy covered nobody.

A roofing subcontractor shows up to your job site with a certificate of insurance in hand. The workers comp section shows a carrier name, a policy number, and dates that are current. You file it. The project starts.

Six weeks later, one of that subcontractor’s workers falls from the roof. The worker has no workers comp coverage. The North Carolina Industrial Commission gets involved. Your attorney gets the call.

You find out the policy on that certificate was a ghost policy. It was real in the narrowest technical sense. But it was structured in a way that left every worker on that job site completely unprotected.

- North Carolina General Statute § 97-19, principal contractor liability

- North Carolina Industrial Commission employer coverage guidance

Check the subcontractor certificate before work starts

Carolina Risk Partners helps North Carolina contractors review workers comp certificates, owner exclusions, payroll, class codes, and subcontractor verification processes.

Best reviewed before the subcontractor starts work.

What Is a Workers Comp Ghost Policy?

A ghost policy is usually issued to a sole proprietor, single member LLC, or small business where the owner has excluded themselves from workers compensation coverage and no other employees are listed.

The certificate of insurance can look exactly like any other workers comp certificate. The carrier name is real. The policy number is real. The effective dates are real. The policy itself was issued.

What the certificate usually cannot show is the real coverage problem: no covered payroll, no covered field employees, and sometimes an excluded owner. For practical claim purposes, the policy may not protect anyone doing physical work on the job.

That is why it is called a ghost policy. The business exists on paper. The policy exists on paper. The coverage for the actual workers may disappear when the claim starts.

Why Ghost Policies Exist in North Carolina Construction

Workers comp premiums for construction trades are often driven by payroll and classification. A roofing crew, framing crew, excavation crew, or tree service crew has a very different workers comp cost than a business with no covered payroll.

For a subcontractor under cost pressure, a low-premium policy can feel like an easy way to satisfy certificate requirements. Sometimes the owner does not fully understand what they purchased. Sometimes they know exactly what they purchased. Either way, the certificate lands on the general contractor’s desk and looks like coverage.

The problem is that the certificate does not tell the whole story.

Why This Is a North Carolina General Contractor Problem

North Carolina gives this problem a legal structure general contractors cannot ignore.

Under N.C.G.S. § 97-19, a principal contractor can face workers compensation liability when a subcontractor does not carry required coverage and a worker is injured while performing the subcontracted work.

In practical terms, if your subcontractor has no real workers comp coverage and one of their workers gets hurt on your project, the claim may move up the chain.

The North Carolina Industrial Commission is not focused on whether the certificate looked acceptable in your file. The practical question is whether the injured worker had workers comp coverage that actually responded.

What a Certificate of Insurance Does and Does Not Prove

This distinction matters more than most general contractors realize.

A certificate of insurance can show:

- that a policy was issued

- the carrier name and policy number

- the policy effective and expiration dates

- the coverage types listed on the certificate

A certificate of insurance usually cannot show:

- whether the owner has excluded themselves from coverage

- whether any field employees are actually covered

- what payroll is listed on the policy

- what workers comp class codes are assigned

- whether the policy would respond to a claim involving the workers on your site

A ghost policy clears the first list. It fails the second list. That is the danger.

Ghost Policy Warning Signs Before a Claim Happens

There is no single line on a certificate that proves a ghost policy exists. But several patterns should trigger a closer review before work begins.

How to Verify Workers Comp Coverage in North Carolina

Accepting a certificate is not the same as verifying coverage. A practical verification process should happen before the subcontractor starts work.

How to verify coverage before work starts

Policy. Confirm the policy is active with the carrier.

Exclusions. Ask whether the owner or officers are excluded.

Payroll. Confirm whether covered payroll exists.

Class codes. Check whether the classifications match the work.

Notes. Document the date, person, and answers.

Step 1: Confirm the policy is active

Call the carrier listed on the certificate. Do not rely on the certificate dates alone. Ask the carrier to confirm the policy is current and in good standing as of the date the subcontractor is scheduled to begin work.

Step 2: Confirm who is excluded

Ask specifically whether the named insured, owner, members, partners, or officers have elected to exclude themselves from coverage. This is often the fastest way to uncover the ghost policy problem.

Step 3: Confirm covered payroll and class codes

Ask what payroll is currently listed and which class codes apply. A subcontractor with a roofing crew and zero payroll on the policy should not be treated as a subcontractor with real workers comp coverage for that crew.

Step 4: Request a declarations page

A declarations page can help show the policy period, named insured, classifications, estimated premium, and other key details. Review it alongside the certificate.

Step 5: Document the verification call

Write down the carrier contact, the date and time, the person you spoke with, and what they confirmed. If a claim surfaces later and coverage is disputed, your verification record may matter.

Need a better subcontractor verification process?

Send the certificate or your current onboarding process. We can help identify where ghost policies, owner exclusions, payroll gaps, and class code mismatches may slip through.

What Happens When a Ghost Policy Surfaces After an Injury?

When a worker is injured and the subcontractor’s policy turns out to be a ghost policy, the claim can become complicated quickly.

The injured worker may file with the North Carolina Industrial Commission. The Commission and the carriers involved will evaluate whether the subcontractor had coverage that actually applied to the injured worker.

If the subcontractor had no real coverage, the general contractor may be pulled into the analysis under N.C.G.S. § 97-19. At that point, general liability is usually not the clean solution. General liability is built for third-party bodily injury and property damage. It is not designed to replace workers compensation.

Depending on the facts, your own workers comp carrier may also review whether uninsured subcontractor labor creates premium, audit, or claim exposure. These situations are fact-specific and should be reviewed with your broker and legal counsel.

What We Check in a Subcontractor Workers Comp Review

Carolina Risk Partners helps general contractors build a practical process for reviewing certificates and identifying ghost policy red flags before a claim forces the issue.

What General Contractors Should Require Before Work Begins

The certificate of insurance should be the start of verification, not the end of it. Your subcontractor onboarding process should reduce the chance that a ghost policy slips through.

- Require a current certificate of insurance before work begins.

- Request a declarations page when the subcontractor has field labor.

- Verify active coverage directly with the carrier when the risk is significant.

- Ask whether the owner or officers are excluded.

- Confirm that covered payroll and class codes match the work.

- Document your verification call and keep notes in the subcontractor file.

- Track expiration dates and re-verify at renewal.

- Use written subcontractor agreements that require real workers comp coverage.

Why Ghost Policies Are Part of a Larger Subcontractor Verification Problem

Ghost policies are one version of a broader issue: the coverage shown on paper may not match the coverage that actually exists when a claim happens.

That same gap can appear with lapsed policies, incorrect class codes, excluded owners, uninsured 1099 labor, missing additional insured endorsements, and subcontractors who were legally small enough to avoid workers comp but still created project risk.

North Carolina’s workers comp rules can also be misunderstood. The three-or-more employee rule is important, but contract requirements and job site risk can be stricter than the legal minimum. A subcontractor may not think they need workers comp, but the general contractor may still need proof of coverage before allowing them onto a project.

How Carolina Risk Partners Helps Contractors Avoid Ghost Policy Problems

Carolina Risk Partners helps North Carolina contractors review workers compensation, subcontractor certificates, owner exclusions, payroll classifications, audit exposure, and certificate verification procedures.

We are not a law firm and do not provide legal advice. But we can help identify when an insurance certificate does not answer the questions a general contractor actually needs answered.

Frequently Asked Questions

What is a workers comp ghost policy?

A workers comp ghost policy is a real workers compensation policy issued to a business with no covered employees. It may produce a valid certificate of insurance, but it may not cover the owner or the workers performing labor on a job site.

Are ghost policies illegal in North Carolina?

The policy structure itself is not automatically illegal. Some owners can legally exclude themselves from workers compensation coverage. The risk begins when a certificate from that policy is accepted as proof that job site labor is actually covered.

Can a North Carolina general contractor be responsible if a subcontractor has a ghost policy?

Yes. Under N.C.G.S. § 97-19, a principal contractor can face workers compensation exposure when a subcontractor does not carry coverage that responds to an injured worker’s claim. The exact outcome depends on the facts and should be reviewed with legal counsel and an insurance professional.

Does a certificate of insurance prove that subcontractor workers are covered?

No. A certificate of insurance can show that a policy exists, but it usually does not prove who is excluded, what payroll is listed, what class codes are used, or whether the workers on the job site are actually covered.

How can a general contractor verify workers comp coverage?

A general contractor should call the carrier, confirm the policy is active, ask who is excluded, confirm payroll and class codes, request a declarations page when appropriate, and document the verification call before the subcontractor starts work.

Does general liability cover an injured subcontractor worker when workers comp is missing?

General liability is generally not a substitute for workers compensation. If a subcontractor’s worker is injured and the subcontractor has no real workers comp coverage, the claim may involve statutory workers compensation exposure, contractual issues, and fact-specific coverage analysis.

Stephen Ellias is the founder of Carolina Risk Partners LLC, an independent commercial insurance agency based in Wake Forest, North Carolina. He is a licensed North Carolina insurance professional, license number 20374040, with a CLCS, Commercial Lines Coverage Specialist, designation. Stephen helps general contractors, trade contractors, and blue-collar businesses understand workers compensation, subcontractor verification, audits, general liability, commercial auto, umbrella liability, and contract insurance requirements in a clear and practical way.

Do not let a ghost policy become your workers comp problem.

Carolina Risk Partners helps North Carolina contractors review workers comp certificates, owner exclusions, payroll, class codes, subcontractor files, and audit exposure before a claim exposes the gap.

Not ready for a quote? Ask us to review your subcontractor certificate process first.