Experience Modification Rate in North Carolina Workers Comp: How Your EMR Is Calculated

A practical guide to what your workers comp mod means, why it follows your business, and what can move it up or down before renewal.

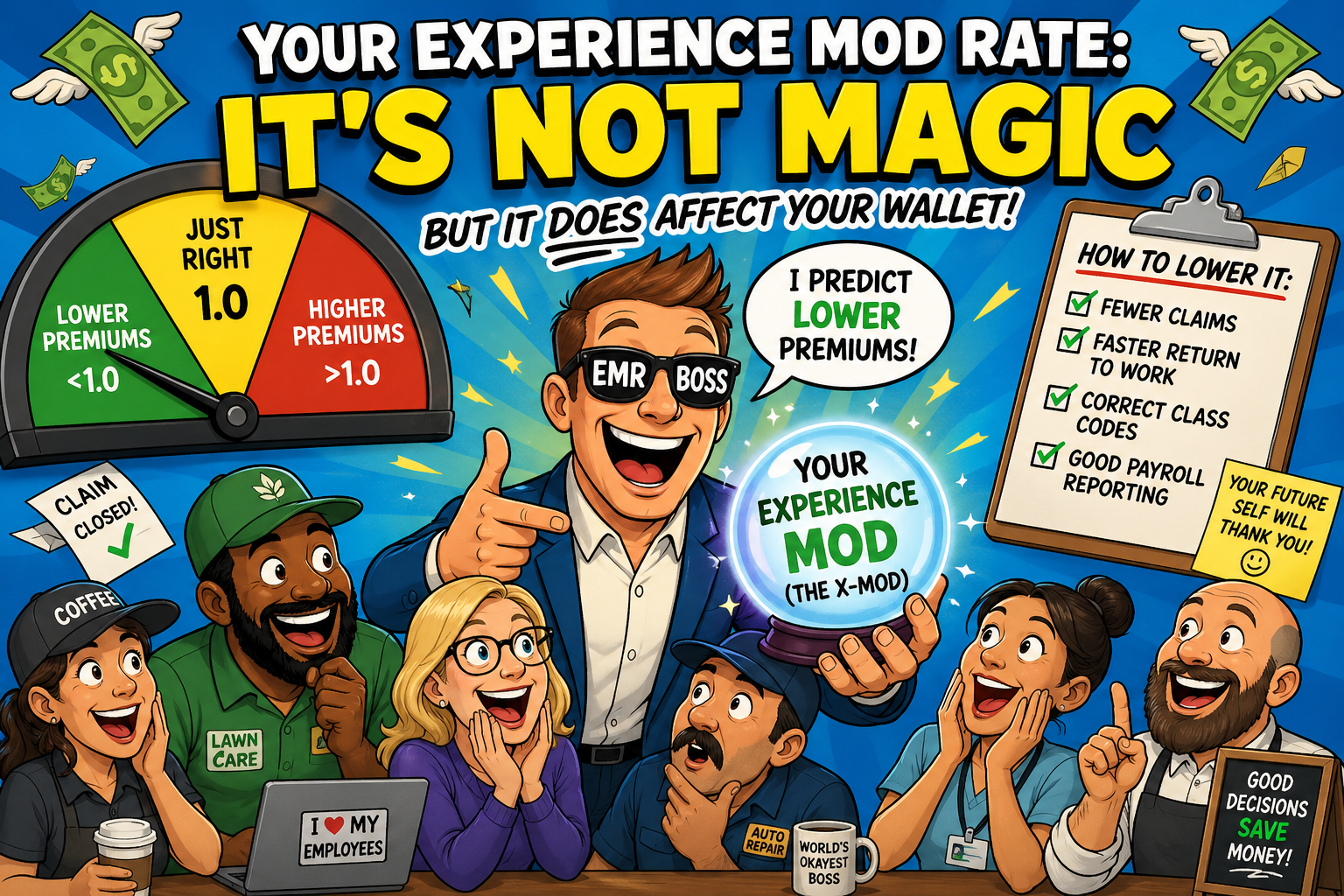

- Your EMR compares your actual workers comp losses against expected losses for businesses like yours.

- NCCI calculates experience mods for qualifying North Carolina employers using payroll, class code, and loss data.

- The experience period generally uses three prior policy years, but excludes the most recent completed year.

- Several small claims can hurt your mod more than one larger claim because claim frequency is heavily weighted.

- Open claims, high reserves, misclassified payroll, and poor return-to-work practices can push your EMR up.

- A high EMR can affect workers comp premium and eligibility for certain construction, municipal, and commercial contracts.

Your experience modification rate, often called EMR, X-Mod, or experience mod, is a workers compensation pricing multiplier. A 1.00 mod is average. A 1.25 mod can increase your workers comp premium by about 25 percent before other credits or debits. A 0.80 mod can reduce it by about 20 percent.

Bottom line: your EMR can affect premium, renewal strategy, and contract eligibility, so it should be reviewed before renewal instead of after the quote lands.

The experience modification rate in North Carolina workers comp is not just an insurance number. For contractors, manufacturers, staffing companies, landscapers, healthcare employers, and other businesses with field or operational employees, it can affect premium, renewal options, contract eligibility, and how underwriters view the account.

If your business has a 1.00 mod, you are at unity. That means your workers comp premium is not being increased or decreased by the experience mod itself. If your business has a 1.25 mod, your base workers comp premium may be increased by about 25 percent before other credits, debits, expense constants, and carrier adjustments. If your business has a 0.80 mod, your premium may be reduced by about 20 percent before those other rating factors.

NCCI compares your actual losses to the losses expected for your industry, payroll, and class codes. Better-than-expected loss experience can push your mod below 1.00. Worse-than-expected loss experience can push it above 1.00.

What the Experience Modification Rate Actually Is

Your experience modification rate is a multiplier applied to your workers compensation premium. It may appear on your policy, worksheet, proposal, or renewal documents as EMR, X-Mod, experience mod, mod factor, or experience rating modification.

The idea is simple. Two businesses may have the same class code and payroll, but their safety records may be very different. Experience rating gives a financial reward to businesses with better-than-expected loss experience and a financial penalty to businesses with worse-than-expected loss experience.

For example, if your manual workers comp premium is $40,000 before the mod:

- A 0.85 mod can reduce the premium impact by about 15 percent before other adjustments.

- A 1.00 mod keeps the premium at unity before other adjustments.

- A 1.25 mod can increase the premium impact by about 25 percent before other adjustments.

That difference compounds quickly. A business that carries a high mod for several years may spend tens of thousands more than a similar business with cleaner claims experience.

Who Calculates the EMR in North Carolina?

For qualifying North Carolina employers, the experience modification rate is calculated through the National Council on Compensation Insurance, commonly called NCCI. NCCI collects payroll and loss data reported by workers compensation carriers, applies the experience rating formula, and produces the mod used by the carrier.

The North Carolina Rate Bureau, often called NCRB, also plays an important role in North Carolina workers compensation rating, rules, filings, and state-specific administration. The North Carolina Department of Insurance regulates the insurance marketplace, while the North Carolina Industrial Commission administers the Workers Compensation Act and handles disputes involving workers compensation benefits.

The key point for business owners is this: your mod does not reset just because you switch insurance carriers. The mod generally follows the business experience, payroll, losses, and ownership history. A new carrier still has to use the applicable experience rating data.

Switching carriers may change your premium, underwriting appetite, payment options, deductible options, or schedule credits. But it does not usually erase the loss history feeding your EMR.

Want your EMR reviewed before renewal?

If your workers comp renewal is coming up, send the basics and I can help identify what may be driving your mod.

Do not send private claim documents through this form. I can tell you what to gather next.

Which Businesses Receive an Experience Modification Rate?

Not every business receives an EMR. Experience rating usually applies once a business meets the applicable premium eligibility threshold for the rating period. Smaller employers may not generate enough premium volume to qualify.

Businesses that commonly become experience rated in North Carolina include:

- General contractors and specialty trade contractors

- Roofing, electrical, plumbing, HVAC, and framing businesses

- Landscaping and tree service companies with crews

- Manufacturing and warehouse operations

- Staffing agencies with industrial or field placements

- Healthcare facilities and home health businesses

- Restaurants, hospitality groups, and larger retail employers

Eligibility depends on current rating rules and premium size. Your broker can confirm whether your business qualifies by reviewing your workers comp history and NCCI experience rating data.

How the EMR Formula Works

The full NCCI formula has several moving parts, including expected loss rates, discount ratios, weighting values, ballast values, class code payroll, and reported claim data. Business owners do not need to memorize the formula, but they do need to understand the mechanics.

The experience period

The experience rating calculation generally uses three prior policy years of payroll and claim data. The most recent completed policy year is usually excluded because claims from that year may not be fully developed yet.

For example, if your policy renews in 2026, the mod may be looking at older policy years such as 2022, 2023, and 2024, depending on your specific effective date and rating period. Your broker can obtain the unit statistical report or experience rating worksheet to show exactly which years are feeding the current number.

Actual losses versus expected losses

NCCI assigns expected losses based on your payroll and workers comp class codes. A roofing contractor with $1 million of field payroll is expected to produce more losses than a clerical office with $1 million of payroll because the work is physically riskier.

If your actual losses are lower than expected, your mod can move below 1.00. If your actual losses are higher than expected, your mod can move above 1.00.

Primary losses versus excess losses

One of the most important concepts in the formula is the split between primary losses and excess losses. NCCI divides claim values into different buckets. The primary portion of a claim carries more weight in the formula. The excess portion carries less weight.

That means claim frequency often matters more than most business owners realize. Several smaller claims can hurt your mod more than one larger claim of the same total value because repeated primary losses signal a pattern.

A business with six small claims may take a harder mod hit than a business with one large claim of similar total value. The formula is built to penalize frequency because repeated claims suggest a recurring safety or claims management issue.

The EMR and the 1.5 Threshold in North Carolina

A high mod is already expensive, but in North Carolina the 1.5 threshold deserves special attention.

North Carolina employers with an experience rate modifier of 1.5 or higher may be subject to state safety and health program requirements. That makes a 1.5 mod different from a normal pricing issue. It can become a compliance issue, a safety management issue, and an underwriting issue at the same time.

If your EMR is approaching 1.5, this should not wait until renewal week. It is worth reviewing open claims, loss runs, payroll classifications, safety practices, and return-to-work options as early as possible.

The Connection Between Class Codes and Your EMR

Your workers comp class codes affect both sides of the calculation.

First, they affect your base workers comp rate per $100 of payroll. Second, they affect the expected losses that NCCI uses to compare your business against similar operations.

If payroll is misclassified, the problem can show up in multiple places. Office payroll coded as field payroll can overstate the risk and increase premium. Hazardous work coded under a cheaper class can create audit exposure, underwriting problems, and retroactive premium issues.

Construction example

A contractor that does not separate clerical payroll from field payroll may overpay and distort the data feeding the account.

Landscaping example

A company that mixes office staff, lawn crews, and tree service work under one classification may create audit and rating problems.

Staffing example

A staffing agency that mismatches employees to the wrong job duties may create major class code and premium problems.

Healthcare example

A business with clinical and administrative staff needs clean payroll separation so lower-risk duties are not blended into higher-risk work.

What Moves Your EMR Up?

Understanding what pushes the mod higher is the first step toward controlling it.

Frequent claims

Several small claims can be worse for your EMR than one isolated larger claim. The formula is sensitive to frequency because repeated claims suggest a pattern that may continue.

Open claims with high reserves

Open claims can carry reserves that feed into the experience rating data. If reserves are too high or claims remain open longer than necessary, your mod may be affected even before the claim is fully paid and closed.

No return-to-work process

Lost-time claims usually create bigger reserves than medical-only claims. If an injured employee stays completely out of work when modified duty could have been offered, the claim can become more expensive and more damaging to your mod.

Payroll reporting mistakes

Bad payroll estimates, poor audit records, and incorrect class code splits can affect both premium and expected loss calculations.

Unreviewed claims

Not every reported injury is automatically compensable. Claims should be reviewed promptly and handled through the proper workers compensation process. If questionable claims are accepted without investigation, those losses may stay in the experience period for years.

What Moves Your EMR Down?

The same mechanics that push the EMR up can work in reverse.

Clean claims years

A clean claims year helps because the experience window rolls forward. Older bad years eventually drop out, and better years begin to replace them.

Active claim reviews

Reviewing open claims with the carrier can help identify claims that may be ready for closure, settlement, or reserve reduction.

Return-to-work planning

A simple modified duty plan can reduce lost-time exposure. The plan does not need to be complicated. It just needs to be written, realistic, and ready before the injury happens.

Class code corrections

If payroll is coded incorrectly, fixing it can reduce premium and improve the accuracy of the experience rating data going forward.

Unit statistical report review

The unit statistical report shows payroll and loss data reported to the rating organization. If the data is wrong, the mod may be wrong. A broker who regularly reviews workers comp accounts should be able to walk through this report with you.

Need the mod worksheet explained?

Most business owners are never shown what is actually driving their EMR. I can help review the worksheet, open claims, class codes, and payroll data before renewal.

No obligation. Just a practical next step.

The EMR and Contract Eligibility in North Carolina

For many contractors and field service businesses, the EMR is not only a pricing factor. It can be a gatekeeper.

General contractors, project owners, municipalities, school systems, healthcare facilities, industrial accounts, and state-related projects may ask for an EMR below a specific threshold. Common requirements may include a mod below 1.00, 1.10, or 1.20, depending on the contract.

If your EMR is too high, you may be disqualified before price, qualifications, safety record, or relationships are even considered. That makes the mod a business development issue, not just an insurance issue.

A high EMR can cost more than premium. It can keep you off bid lists, block subcontractor approvals, and weaken your position with larger project owners.

Why This Matters in Wake Forest, Raleigh, Durham, and the Triangle

In markets like Wake Forest, Raleigh, Durham, Cary, Apex, Johnston County, the Triad, and Charlotte, many contractors and service businesses grow quickly. Growth creates payroll, payroll creates workers comp premium, and premium volume can eventually make the business experience rated.

A company may start as a smaller account with no mod, then add crews, vehicles, subcontractor relationships, and larger contracts. By the time the business starts bidding commercial or municipal work, the EMR may become part of the conversation.

That is why the best time to manage the mod is before it becomes a problem. Claims reporting, payroll separation, return-to-work planning, and claim review habits need to be in place while the business is growing.

Your EMR Reduction Checklist

Use this before your next renewal conversation with your broker.

How Carolina Risk Partners Helps With EMR Reviews

Carolina Risk Partners helps North Carolina contractors and business owners review workers compensation programs before renewal, not just after the premium has already increased.

That review may include:

- Current EMR and prior mod history

- Workers comp class codes

- Payroll splits between field, clerical, and supervisory employees

- Open claims and reserve questions

- Return-to-work options

- Contract requirements tied to mod thresholds

- Audit issues that may affect future rating

If your mod is above 1.00, approaching 1.5, or starting to affect contract eligibility, it is worth having the conversation before the next renewal quote lands.

Frequently Asked Questions

What is a good EMR for a North Carolina business?

A 1.00 EMR is average, also called unity. Anything below 1.00 is generally favorable because it can reduce workers compensation premium before other rating adjustments. Many contractors and larger employers try to keep their EMR below 1.00 because it can affect both premium cost and contract eligibility.

Is a 1.25 EMR bad?

A 1.25 EMR usually means the workers compensation premium is being increased by 25 percent before other credits or debits are applied. It may also create problems with contracts that require a mod below a certain threshold.

Who calculates the experience modification rate in North Carolina?

The National Council on Compensation Insurance, commonly called NCCI, calculates experience modification rates for qualifying North Carolina employers using payroll, class code, and loss data reported by carriers.

Can a broker help lower my EMR?

A broker cannot simply request a lower EMR. However, a broker can review the mod worksheet, look for payroll or class code errors, monitor open claims, coordinate with the carrier on reserves, and help build a return-to-work plan that may improve future mods.

How long does it take to lower an EMR?

The experience modification rate is generally based on three prior policy years of payroll and loss data. A clean claims year helps, but meaningful improvement often takes two to three years of disciplined claims management.

Can I get my EMR lowered before renewal?

Possibly, but usually only if the underlying data is wrong. If payroll, class code, or loss data was reported incorrectly, a correction may result in a revised mod. If the data is accurate, the next scheduled recalculation usually reflects the rolling experience period.

Does my EMR affect general liability premium?

The EMR directly applies to workers compensation premium, not general liability premium. However, poor workers compensation loss history may still affect how some carriers view the overall account.

Does an EMR reset if I switch workers comp carriers?

No. Switching workers compensation carriers does not usually reset the EMR. The mod generally follows the business experience, payroll, losses, and ownership history rather than the insurance carrier.

Stephen Ellias is the founder of Carolina Risk Partners LLC, an independent commercial insurance agency based in Wake Forest, North Carolina. He is a licensed North Carolina insurance professional, license number 20374040, with a CLCS, Commercial Lines Coverage Specialist, designation. Stephen helps contractors and trade businesses understand workers compensation, experience modification rates, class codes, audits, claims management, return-to-work programs, and contract insurance requirements in clear, practical terms.

Need a second look at your EMR before renewal?

Carolina Risk Partners can help review your mod worksheet, workers comp class codes, open claims, payroll records, and renewal strategy before the number becomes more expensive.

Disclaimer: This article is for general educational purposes only and is not legal advice. It does not create an insurance, broker, or attorney-client relationship. Workers compensation rating rules, experience modification calculations, class codes, claims data, contract requirements, and underwriting decisions vary by business, state filing, carrier, and policy history. Speak with a licensed insurance professional about your specific situation.